So you want cheaper insurance. Don’t we all? Whether we’re talking about auto insurance or health insurance, our wallets are squeezed by the real insurance companies while our email inboxes are flooded with a barrage of messages touting better deals. Even if we’re sure that unbelievable insurance offer is a fake, we always wonder, what if it’s real? What could be the harm in checking it out? Let’s see why acting on one of those emails would be a really bad idea.

So you want cheaper insurance. Don’t we all? Whether we’re talking about auto insurance or health insurance, our wallets are squeezed by the real insurance companies while our email inboxes are flooded with a barrage of messages touting better deals. Even if we’re sure that unbelievable insurance offer is a fake, we always wonder, what if it’s real? What could be the harm in checking it out? Let’s see why acting on one of those emails would be a really bad idea.

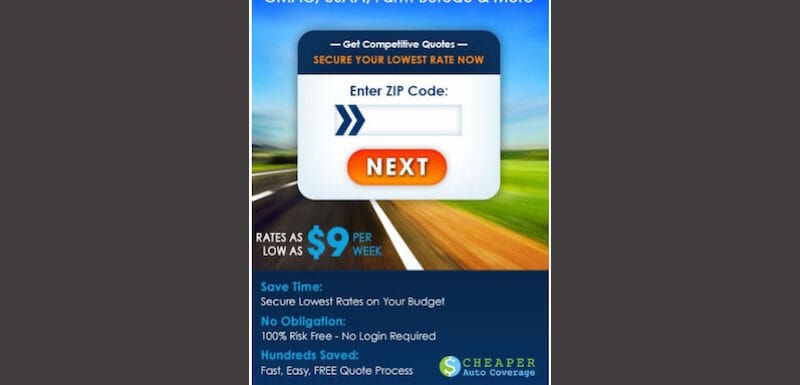

Here’s an example of an offer for “Cheaper Auto Coverage.” First off, let’s take a look at how “cheap” this coverage really is. The email offers rates “as low as $9 per week.” Hmmm, pop quiz, how many weeks in a year? Yup, fifty-two. And, if you’ve done the math and come up with that being equivalent to $468 per year, you can see that we’re not off to a very good start.

That $468 is probably better than your current rate, but here’s the catch. Insurance rates are based on coverage. The minimum coverage you can take is that which is required by law. You can’t really name your price because the rates are negotiated between the insurance company and the regulating authority. If it even exists, that $9 weekly cost would be minimum coverage in the lowest-cost region for a driver with the lowest risk. In other words, it’s the equivalent of new car fuel economy ratings where a manufacturer claims the latest model gets 36 MPG—and you get 12.

All of the above assumes that the insurance offer is even legitimate. The truth is, what you received is quite likely a fake insurance email not even sent by a legitimate provider. For instance, the example I’m using came from an address with a European domain name.

The bottom line is that the email I received is not legitimate. Nor are the mass emails you receive. The pages linked to in the email are designed to deliver malware or steal personal information that you enter to obtain an insurance quote. We’re all so desperate for some sort of relief from insurance costs that ridiculous offers start looking good. Don’t click or call, just drop that email in the trash. Then, shop the legitimate insurance companies. You might just find a lower rate for the same coverage without paying a much bigger price.

Terry- thanks for the info on the ins scam wow I didn’t think of that I don’t carry the lowest limits I know that from working at a big ins co that used to be in the bay area in cust serv and I know that I like to be the one typing the ins co in not replying and sometimes rates may be low but their reaction to other things like accidents etc might be just terrible so you have to check out the whole ball of wax Happy Halloween

How right you are, Peggy. You’ve got to look at everything, not just the price!